My Financial Independence Journey » Investment portfolio » Cardinal Health (CAH) Dividend Stock Analysis

Cardinal Health (CAH) Dividend Stock Analysis

![]() Cardinal Health is a leading wholesale distributor of pharmaceutical products and medical supplies to hospitals, health care centers, and pharmacies. Approximately 91% of its revenue comes from pharmaceuticals and 9% from medical products. In addition to being a wholesaler, the company offers a diverse array of related services. In the UK, Cardinal Health manufactures and distributes generic drugs. In the US, Cardinal Health, repackages and distributes pharmaceutical products for retail and mail order customers, owns the world’s largest network of nuclear pharmacies, and is responsible for the management of over 200 hospital pharmacies that have been outsourced to Cardinal. In 2009, Cardinal spun off Care Fusion, a medical device company. In 2010, Cardinal acquired Healthcare Solutions, an oncology services company. Also in 2010, Cardinal acquired Kinray, a New York drug distributor to a large number of independent pharmacies.

Cardinal Health is a leading wholesale distributor of pharmaceutical products and medical supplies to hospitals, health care centers, and pharmacies. Approximately 91% of its revenue comes from pharmaceuticals and 9% from medical products. In addition to being a wholesaler, the company offers a diverse array of related services. In the UK, Cardinal Health manufactures and distributes generic drugs. In the US, Cardinal Health, repackages and distributes pharmaceutical products for retail and mail order customers, owns the world’s largest network of nuclear pharmacies, and is responsible for the management of over 200 hospital pharmacies that have been outsourced to Cardinal. In 2009, Cardinal spun off Care Fusion, a medical device company. In 2010, Cardinal acquired Healthcare Solutions, an oncology services company. Also in 2010, Cardinal acquired Kinray, a New York drug distributor to a large number of independent pharmacies.

Basic Company Stats

- Ticker Symbol: CAH

- PE Ratio: 14.19

- Yield: 2.5%

- 5 year revenue growth (2008-2012): 4.2%

- % above 52 week low: 96%

- Beta: 0.49

- Market cap: $14.6 B

- Website: www.cardinal.com

CAH vs the S&P500 over 10 years

CAH has been delivering sub-par capital gains for investors over the last 10 year period. By the end of 2012 an investment in CAH would have decreased by about 30%, compared to rising about 60% for the S&P500.

Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: -4.1%

- 10 year EPS growth: -0.2%

- 5 year dividend growth: 15.2%

- 10 year dividend growth: 8.8%

EPS for Cardinal Health appear to be very erratic, bouncing all over the place like an ADHD kid on a trampoline. The dip in 2010 may be due in part to spinning off CareFusion. Unfortunately, the 10 year and 5 year EPS growth rates are negative! Thankfully, the 5 year revenue growth rate is positive.

The dividends are growing at a nice clip. About 15% per year for the last five years. With a dividend growth rate of 15.2% and a current yield of 2.6%, CAH’s yield on cost will grow to about 10% after 10 years.

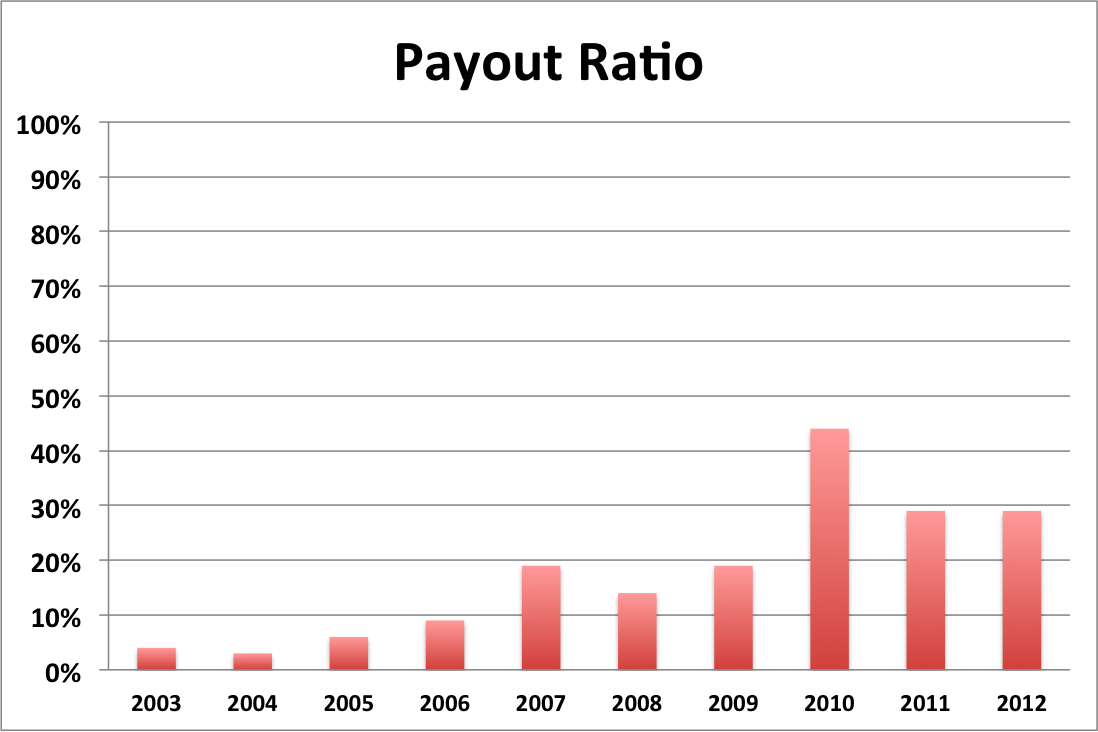

Payout Ratio

With the exception of 2010, CAH’s payout ratio has remained below 30%. The payout ratio has been rising over the years. This is consistent with the consistent dividend increases and the lack of stable EPS growth. The average payout ratio over the last 10 years has been 18%. The lower the payout ratio, the more available cash that the company has to continue to increase dividends or make capital investments. All this suggests that there is plenty of room for CAH’s dividend to grow, assuming that the company can continue to bring in sufficient earnings.

Risks

The nice thing about being a distributor is that the company doesn’t need to repeatedly create innovative like the more well known pharmaceutical companies. Cardinal Health just needs to deliver the drugs. Also, since generic drugs have a higher margin, as drugs come off patent, Cardinal will bring in higher revenues.

Unfortunately the entire pharmaceutical industry as undergone considerable consolidation over the last several years. Cardinal has two major contracts, one with CVS and one with Walgreens, that together account for 43% of Cardinal’s business and are set to expire in 2013. Two of Cardinal’s competitors AmerisourceBergen and McKesson are working hard to steal those contracts away. AmerisourceBergen has already succeded in taking the Express Scripts contact away from Cardinal. Reading recent statements from Cardinal about the contract situation did not inspire confidence.

Graham Number Valuation

The Graham number represents one very simple way to value a stock. The Graham number for CAH is $36.35, which is considerably below the current price of CAH, suggesting that it may be overvalued.

Cash Secured Puts

At this point, I would prefer to hold off on purchasing CAH and would also hold off on selling cash secured puts against it.

Conclusions

Cardinal Health is a very solid company, but if the contracts with CVS and Walgreens don’t come through, expect the market to punish Cardinal severely. If Cardinal makes it through 2013 with it’s revenue intact it might be worth a second look. Overall, it is a stable company with a lot of diversification and a lot of room for growth especially as it continues its efforts to expand into China. But for not, I’m not comfortable making a move.

Cardinal losing one of its contracts could represent a potential buying opportunity if the stock price drops in response. The loss of revenue could slow dividend growth, but it still looks like there is plenty of room for the dividends to grow even with a 20% revenue loss. But if Cardinal Health were to lose two of its contracts, I would wonder whether the dividend could continue to grow at the considerable pace that it has been.

Disclosure: None.

Readers: What are your opinions about Cardinal Health?

Written by myfijourney

Filed under: Investment portfolio · Tags: analysis, CAH, cardinal health

2 Responses to "Cardinal Health (CAH) Dividend Stock Analysis"

Leave a Reply

I agree with your assessment. It sounds like they are overly dependent on a couple of key contracts which may be influenced by price cuts? That seems like a fairly weak economic moat to me, but perhaps there are other factors that determine contract success. I also would be concerned about potential consolidation across pharmacy chains, which may squeeze them even further.

Integrator,

The retail pharmacy consolidation has been going on for years. It started with chains buying up independents, then bigger chains buying smaller ones. Cardinal, while a descent company, is going to have a lot of challenges with other companies being willing to underbid it.