My Financial Independence Journey » Stock Analysis » Intel Corporation (INTC) Dividend Stock Analysis

Intel Corporation (INTC) Dividend Stock Analysis

![]() Intel Corporation is the world’s largest chip maker for microprocessors and personal computers and has been a major player in the business for years. The company has three main business segments. 1) PC client group, which focuses on making chips, chipsets, and motherboards for notebook and desktop computers. 2) Data center group, which focuses on chips, chipsets, and motherboards for servers, storage, data centers, cloud computer, etc. 3) Other Intel Architecture, which focuses on chips for mobile devices, and other consumer electronics.

Intel Corporation is the world’s largest chip maker for microprocessors and personal computers and has been a major player in the business for years. The company has three main business segments. 1) PC client group, which focuses on making chips, chipsets, and motherboards for notebook and desktop computers. 2) Data center group, which focuses on chips, chipsets, and motherboards for servers, storage, data centers, cloud computer, etc. 3) Other Intel Architecture, which focuses on chips for mobile devices, and other consumer electronics.

Basic Company Stats

- Ticker Symbol: INTC

- PE Ratio: 9.24

- Yield: 4.25%

- 5 year revenue growth (2007-2011): 8.9%

- % above 52 week low: 19.2%

- Beta: 1.1

- Market cap: $103.3 B

- Website: www.intel.com

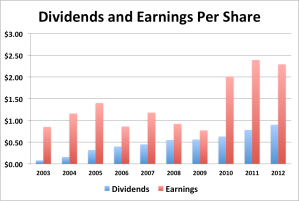

Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: 25.6%

- 10 year EPS growth: 11.6%

- 5 year dividend growth: 13.1%

- 10 year dividend growth: 30.9%

EPS has fluctuated over the last decade, with a slump seen from 2006 to 2009. The slump has several causes including increased competition from rivals such as AMD, the slow entry of Intel into mobile markets (smart phones and tablets) and the Great Recession.

Intel has consistently raised dividends for the last 10 years, which suggests that the company may be maturing into a stable dividend producing investment. Dividend growth thus far has been very aggressive and is likely to slow as the company continues to mature as a dividend growth stock. If dividend growth stays above 10% it will take about 7 years for the dividend to double.

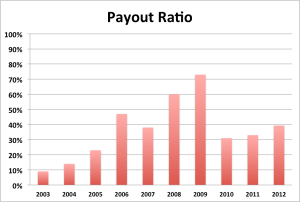

Payout Ratio

Intel’s payout ratio has fluctuated over time. With the exception of 2008 and 2009, the payout ratio has remained below 50%, and usually below 40%. This is a positive sign as it leaves lots of room for future dividend growth. The 10 year average payout ratio is 37%.

Cash Secured Puts

Given my overall favorable opinion of Intel and the fact that it’s current price is only 15% above the 52 week low, I would consider selling long term cash secured puts.

Risks

Intel does have some risks. The most worrisome to me being it’s rather pathetic showing in the mobile arena. As tablet and smartphone sales increase, PC and notebook sales may slow, thus leading to reduced revenue. Also, as Intel continues to dawdle in the mobile space competing companies will continue to improve their products and solidify their products, making expansion into this market more difficult.

Intel is making efforts to gain a larger market share in the mobile arena, however it is still too early to see if these efforts will be successful.

Conclusions

Currently, Intel has several features that make it a particularly attractive buy, including high yield (>4%), a 10 year history of rising dividends, prices near it’s 52 week low, and a consistently low payout ratio (~37% on average).

I would consider adding to my current position in INTC buy purchasing additional shares. I would also consider writing cash-secured puts against INTC.

Disclaimer: I am currently long on INTC. I am also considering writing INTC long term cash secured puts in the next month.

Readers: What are your opinions about Intel?

Written by myfijourney

Filed under: Stock Analysis · Tags: analysis

5 Responses to "Intel Corporation (INTC) Dividend Stock Analysis"

Leave a Reply

I currently have INTC in our (small) dividend portfolio. I like the yield and I understand the technology. I was considering adding more shares and also eyeing LNCO as a buy sometime soon.

Great post! I’m new to dividend growth investing and before I get started, I’m trying to read up on all that I can. Intel is on my list so thanks for the information.

Terah,

Thanks for stopping by. Keep reading everything you can about dividend growth investing. Move into positions gradually. If you make a mistake along the way (I’ve made a few), just try to learn from it and keep pressing forwards.

I’m a little leary on Intel for their poor showing to date in mobile that you highlighted above. My thesis is that their core PC business will start showing strain/decline in the next 2-3 years. Having said that, their dividend payout ratio can be comfortably increased from where it is, and their top line revenue growth and margin is still surprisingly strong, so for the near term they may still be ok as far as dividend growth goes.

Integrator,

I’m a bit worried about Intel and the mobile space too. But they’re a heavyweight and if they set their eyes on something, they’ll probably get there. I remember doubting that Microsoft could make a video game system, and they proved me wrong with the XBox. So maybe it will be the same with Intel.

I’m also not sure if the core PC business will decline or not. It looks like the current trend among home users is tablets and phones. But at some point, corporations are going to have to upgrade their aging PCs, a job which has been mostly delayed due to the recession. And tablets, while cool, are kind of useless for most things other than media consumption.