My Financial Independence Journey » Reflections » Secrets of Super Savers Revealed

Secrets of Super Savers Revealed

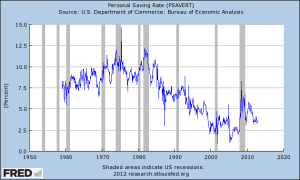

Currently, the average savings rate in the US is pathetically low, somewhere below 5% (3.6% when I wrote this). That means that people are saving, on average, 3.6% of their disposable (after tax) income. I like graphs, so let’s take a quick look at the one on the right. Three things pop out to me. 1) Before 1980 or so people saved around 8-10% of their disposable income. 2) After the early 1980s the savings rate started slowly dropping, and dropping, and dropping. 3) Savings rates spike during recessions.

Currently, the average savings rate in the US is pathetically low, somewhere below 5% (3.6% when I wrote this). That means that people are saving, on average, 3.6% of their disposable (after tax) income. I like graphs, so let’s take a quick look at the one on the right. Three things pop out to me. 1) Before 1980 or so people saved around 8-10% of their disposable income. 2) After the early 1980s the savings rate started slowly dropping, and dropping, and dropping. 3) Savings rates spike during recessions.

So then what’s the difference between super savers (those with double digit savings rates) and the average person? And how can all of us work to boost our savings rate?

I’ve always been fascinated by people on both ends of this savings spectrum. On one end, we’ve got people who burn every dollar they get and then borrow money to burn more. On the other end we’ve got people who save 30%, 40%, 50%, or more of their income.

Principle 1: Having a high income helps you become a super saver, but it’s not required.

Savings rate by income quintile are shown below(*). Remember that each quintile represents 20% of the population.

- Quintile 1 (0-20K/year): 0.3% savings rate

- Quintile 2 (20-38.5K/year): 2.8% savings rate

- Quintile 3 (38.5-62.4K/year): 6.4% savings rate

- Quintile 4 (62.4-101K/year): 6.2% savings rate

- Quintile 5 (101K+/year): 11.9% savings rate

The top and bottom quintiles make sense. If you don’t make much money, you can’t save very much. If you make tons of money, it’s pretty easy to shovel some into savings. What the hell is wrong with quintile 4? They make more, but save less than quintile 3.

What’s interesting is that none of these savings rates are mind blowingly high and super savers can be found in each income quintile.

When I was in quintiles 1 and 2 (grad school), my savings rate was probably around 2%. It took my entire research stipend just to live a modest life complete with a crappy apartment and walking to school every day. I also wasn’t very well versed in the ways of personal finance back then. When I moved to quintile 3 (post doc training) I saved around 25-30% of my salary. Now that I’m in quintile 5 (real job), I’m trying to save 50%+.

Principle 2: Living in a lower cost of living area allows you to save more money, but it’s not required.

Swiped from the Missouri Economic Research and Information Center (MERIC).

Cost of living is a huge determinant in how much you can save. Different areas have radically different costs of living. The higher the cost of living, the more it costs for the basics (food, shelter, utilities, transportation) and the luxuries. Higher cost of living areas often come with higher paying jobs, but the pay increase isn’t necessarily enough to equal everything out.

Check the map on the left to see where your state puts you. Of course, within states cost of living varies widely as well. The cost of living in Chicago IL is way higher than that in Springfield IL. Which brings us to the next principle of being a super saver.

I’ve lived in high and low cost of living areas. And yes, it is way easier to save money when you don’t have to pay through the nose for a one bedroom apartment.

Principle 3: The more modestly you are willing to live, the more you can save.

You don’t necessarily have that much power to immediately change your income or cost of living. You can work to grow your income or look for jobs in cheaper areas of the country, but that takes time may not even be realistic or desirable.

But there is one aspect of your finances that you have a great degree of control over, and that is your lifestyle. The more that you want to live large the less that you’re going to be able to save. I don’t advocate renting an apartment in some slum populated by drug dealers, hookers, and weekly shootings just to save money. Nor do I recommend surviving entirely on lentils and ramen because they’re cheap. On the other hand, just because you graduated college, doesn’t mean that you need to buy a Lexus. Nor do you need a six bedroom house for a family of 3.

Sit down, look at your budget and make some thoughtful decisions about how much you want to spend on what. Everyone deserves to have some luxuries in their life and everyone has things that they don’t care that much about. Try to match your budget to your priorities and save the rest.

I live in modest luxury. I have a nice one bedroom apartment. I could rent something bigger, but at this point in my life I don’t need that much space. I drive an old, but reliable car, which I intend to keep driving until it finally gives up the ghost. I love food, so I spend a lot on it, both cooking and eating out. I also like to travel and explore so I budget for that. Those are my choices that I consciously made budgeted accordingly for. The worst situation is when you are just reactive, buying whatever you want at the moment because it’s there, without any regard for how it fits into your overall personal and financial goals.

Principle 4: External financial burdens affect how much you can save.

Sometimes we have financial commitments that we may or may not have ever wanted in the first place.

Perhaps we have to take care of kids, non-working spouses, or our aging parents. These circumstances can bring us joy and happiness, but they also cost money and thus limit our savings.

Then there is all kinds of debt – consumer debt, mortgage debt, and student loan debt. Consumer debt is the most onerous of the three, because of the high interest rates and the fact that you probably didn’t need to buy any of that crap in the first place. Mortgage debt is a problem if you buy way more house than you need. The more money you put into housing payments, the less you have left over to build passive income streams. Then there are student loans. These can be great investments if the result is a high paying job that you love. Or terrible investments if the result is no job or a career that you hate.

Currently, I have no financial commitments. A fact that I am very thankful for.

In summary:

If you want to become a super saver, focus on these four core principles. Everyone’s situation is different, but most of us can and should be saving more. Especially if we want to become financially independent. Every bit of income that we can save is one step closer to achieving financial independence.

- Make a high income (I’d recommend high five figures at least).

- Live in a low cost of living area.

- Keep your lifestyle modest. Live like a new graduate who just got their first job.

- Minimize financial commitments.

(*) This data was kludged together by combining 2011 tax data and a 2004 study by Dynan et al.

Readers: Are you a super saver? Do you want to become one? Do you agree with the four principles proposed here? Would you add any? What are your secrets to saving tons of money?

Written by myfijourney

Filed under: Reflections · Tags: Reflections, saving

33 Responses to "Secrets of Super Savers Revealed"

Leave a Reply

I have always saved a great part of my income, in order to stop working a corporate job as soon as possible. Avoiding lifestyle inflation but like you budgeting for what was important. Now I don’t really know what my savings rate is since I don’t have a day job anymore and live off investments and a few freelance job but with a day job I was well over 50% for sure.

I’ve often wondered if savings comes naturally to some people and not to others. Interestingly, if you’re familiar with the OCEAN personality traits, the C stands for “conscientiousness” and it’s been shown that people who score higher on that particular personality trait tend to save more. One day I need to dig that study up and write about it.

I would say savings is a natural skill some people possess. You can overcome lack of this skill with mental conditioning as DM says below. I know I’m not a natural saver per se, but I love being at home so much that I simply don’t spend money on very much. Being a natural homebody has been how I’ve saved my paychecks.

Home,

Thanks for stopping by. Being a homebody can lead to impressive savings. But not necessarily. If you’re a homebody who stocks his or her house with all kinds of fancy expensive things (iAnything) and has expensive hobbies, savings can dwindle.

And just because someone may like getting out of the house, doesn’t make them a spendthrift. But if you’re not a homebody, you do need to keep a solid focus on your priorities, otherwise, there’s just too many easily available ways to blow through your earnings.

I’m intrigued about the OCEAN, and briefly looked it up, I have reversed conscientiousness and am messy/disorganized in most areas of life. I think most of my financial behavior came from my parents who had severe stigma from growing up post WWII in Europe. Food was still rationed years after the war and they had to be thrifty and kept that even after they were well off. Maybe they bent my conscientiousness just financially!

Your upbringing certainly affects your behavior. I have lots of little quirks inherited from my parents. It’s funny because everything that I said was stupid as a child and insisted that I would never do as an adult (the house must be clean before you travel) — I am now doing reflexively. I still think it’s stupid, but it’s like a habit.

I can see frugality being in the same vein. My parents were pretty cheap. I’m not as cheap as them, but I’m still cheap compared to my peers.

“I’ve often wondered if savings comes naturally to some people and not to others.”

I wonder this too sometimes.

This may be surprising, but it certainly doesn’t come “naturally” to me. Up until a few years ago I spent almost every dime I had ever earned. I’m a good saver now because I see greater benefit from the saved capital than I do from spending it and receiving goods/experiences now. It’s the greater purchasing power/time that I’ll receive in the future that I’m choosing over the lesser purchasing power/time now.

Like anything in life there has to be a great reason to do this, to save. If there is no significant motivation for it, then why do it right? Then again, maybe it does just come natural to some others in which case the saving in itself is the reward.

Best wishes!

I’m at a strange mid point. I want to save money and I want to spend it. I think being raised by cheap parents and graduating during the crash really solidified the need to save money for me and having a few lousy bosses and work environments drove me towards early financial independence.

But the reality when I look at it rationally is that I could probably knock my savings rate down to 20-25%, retire in 30 years like everyone else and buy a lot more stuff. My fears about layoffs and bad bosses are probably overblown.

But on the other hand, if I pull off early financial independence, I’ll have at lot more options open to me in the future. And a lot less stress when things go South. I like that feeling of security.

Unfortunately if the past is an indicator of the future, the savings rate will be creeping back down once the economy turns for the better. It’s funny how quickly things turn and people just forget what things were like just a few short years ago and how much better off they’d have been had they had more savings. Of course the government continually extending the unemployment benefits kind of dulls the memory.

I think that savings does come naturally, it’s one of nature’s yin and yang things. You have extroverts and introverts. Savers and spenders. Right brain and left brain thinkers.

One of the biggest points from your post is that you need to prioritize your budget to spend on the things that you truly enjoy and cut the rest to the bare minimum that you can live with.

I’m inclined to agree with you. Once the economy improves, it’s likely that people will go back to being spendthrifts.

Prioritization is big for me. I probably over-think it more times than not. But I like to imagine that this way of thinking helps me get the most value for my money and still lets me live large in the areas that matter to me.

It is nicely spell out article. That let me stop a bit and thinking. Although i am in the 3rd quintile am am saving like those in 5th one. However, currently unable to save more than 10% of my income. Also I am not sure whether you can get high income paying job in a low cost (and mostly low income) locations. At least in many common professions. So for most of the population this would be hard to achieve.

Martin,

Thanks for stopping by. If you’re already saving 10% of your income, you’re doing way better than most Americans.

I don’t know the specifics of your situation, but there are two basic ways to save more money – either cut back on expenses or find a way to make more money. If you want to achieve financial independence, you’ll have to examine your situation and try to find out what will work for your situation.

But so long as you’re saving, investing, and trying not to waste your money thoughtlessly, you’re doing so much better than most of the population.

MFI, I live in a very expensive area. It is a ski resort and although I could find a well paid job here as a mechanical engineer, the cost of living is so high that it offsets my income significantly. The apartment I have bought a few years ago was so expensive that for the same amount I could buy a large mansion elsewhere. I also tried to find another job in my field in cheaper area and mostly the job offers couldn’t match what I am making now. But I see one thing I could do to save more and that is to get rid of the debt I carry. Although I am paying it off, no doubt, it is slow process, but once done, I’ll have a very significant amount of money available to invest.

Definitely keep working on knocking out your debt. Hopefully as the economy improves, more jobs will open up and you’ll be able to find a comparable job in a lower cost of living area. Just don’t get discouraged and keep looking around. Opportunities often arise when you least expect them.

As you correctly point out, the existence of financial commitments with supporting children can send your savings rate tumbling (especially during the early infant stage). I’ve experienced this first hand myself!

Having said that your upbringing likely plays a big point in your attitude to saving, and even with a young family, we still save a substantial portion of our income. In my view, upbringing is possibly the defining factor in terms of an inherent “willingness to save”. Like you, my parents were also incredibly careful with money. There were really “super savers”. You don’t have to learn to save in these circumstances. Its a conditioned behaviour. You just do it!.

I think making an automatic process of having a certain amount of your paycheck go direct to stocks or a savings account can help make saving much easier. If you don’t see it, you don’t know its there, and you won’t be tempted to touch it.

I don’t have any payments automated. But I do make budgets out at the beginning of the year and pretty clearly lay out where I want my income from each month to go. Then I just try my best to keep my expenses down. Sometimes I succeed, sometimes not so much.

One thing to consider that these stats are after tax. Someone could only be saving 3% post tax, but investing 20% pre-tax.

Ginger,

Thanks for stopping by. Disposable income is total personal income minus personal current taxes. Savings rate is calculated based on disposable income. The number doesn’t discriminate between pre-tax and post-tax accounts. It’s just total money saved divided by total money left over after taxes.

From what data I’ve seen so far, it doesn’t matter if you look at specifically pre or post tax savings. The end result is the same. Americans are not saving anywhere near enough money to retire.

We have done quite well in savings department. Even with income cut in half we are saving above the average. One thing that really really pushed us to save more when we started saving (we were living paycheck to paycheck until 2009/early 2010 is to have concrete goals. We didn’t save much when the point was to just save. When it translated to we need $x by 2012, which means we have to save $y every month, it became much much easier.

Saving isn’t too hard once it becomes a priority. Trying to push to needlessly extreme levels gets challenging, because almost anything that you do to deviate from the budget knocks your savings percentage down.

The real trick is keeping your spending focused on only those things that matter to you. I could buy tons of stuff, but a lot of it would just wind up in cabinets or closets and then given away when I move.

I agree 100% People should aim to save at least 50% of their take home pay in my opinion. There are so many people who spend money on junk or a house that is too big.

Brick by Brick,

50% is hard for a lot of people to achieve. It’s hard for me. But people really need to do a better job of saving. Personally, I think that many people could cut out a lot of impulse purchases and other junk and wind up saving a ton of money and keeping the same standard of living. With savings rates so low, even small changes will make a huge difference.

I will admit 50% might be a little over zealous but I agree increasing the savings rate from its current number is a must!

but I agree increasing the savings rate from its current number is a must!

I’m on the line between the 3rd and 4th quintile and I save over 50% of my income. I also live in a metro area where living isn’t very cheap. I do it because I want to escape the rat race. I want freedom and the ability to live on my own terms. It’s more important to me that any material good is and when you’re priorities are as such, it’s a no brainer to live like this.

Kraig,

Thanks for stopping by. I want a type of freedom too. Not really from the rat race per say as I like my job a lot. But freedom from having to worry about uncertainty. If I get laid off or if my boss gets replaced by an ogre, I’d like to be able to deal with the situation at my own speed and on my own terms. Unless I’m financially independent, I can’t do that.

I DEFINITELY think savings comes easier to some personality types than others. If you look at the personal finance blogosphere, it is TOTALLY DOMINATED BY ENGINEERS AND COMPUTER PROGRAMMERS. Those folks are usually the Myers-Briggs INTJ personality type. This is the personality type that is also most likely to retire early.

Yes, you are totally correct about the fact the savings rate will probably drop. It actually already has dropped from about 6% a few years ago. It amazes and frustrates me how quickly people can go right back to the kind of spending that got them in trouble in the first place.

Yes, this is what I was thinking. High paying jobs and low cost locations often don’t go together; although I’m sure there are exceptions.

Upbringing definitely helps. But even for kids raised in the same family, some can be big savers while others spend everything they make. There are a lot of factors involved. That said, I am glad my parents always emphasized saving and avoiding debt.

I am in the middle of quintile 3 in a high cost area and I save about 30% of my gross salary (between both retirement and non-retirement contributions), I like my job but my motivation have the same motivation of not being subject to the whims of the job market. Jobs become obsolete very quickly these days and getting more eduction and training for the next job is difficult and expensive. I’ve also seen and read about too many people who lose good paying jobs in their 50s who are never able to make the same kind of money in the next job they find. I won’t be able to retire at 45, but I should be able to retire by my mid 50s, earlier if I moved to a lower cost location.

*Note: I consolidated your comments, for easier reading and replying.**

Engineers and computer programmers work with numbers on a regular basis. Anyone who is unafraid of numbers can pretty easily crank out the math to see how savings affects retirement. I’d love to comment on the Myers-Briggs personality test, but sadly it’s not used in actual studies. The OCEAN scale is more popular and much more robust for psychological research. I do remember reading somewhere that people who score high on Conscientiousness (the C in OCEAN)* tended to be much better savers. No idea if they are predominantly early retirees.

There are always exceptions, they’re just hard to come by.

My parents were pretty good role models for not spending money and staying out of debt. Unfortunately, they were also good role models for being so cheap that it adversely affects happiness. I’m still working on finding appropriate balance.

There are so many reasons to try and achieve financial independence, even if you love your job. For me, financial independence is a kind of insurance. I really enjoy my job, but I’m entirely aware that it may be ripped out from under me at a moment’s notice. Surprise! The company just got acquired and your whole department was downsized! That’s a very real possibility in my industry.

(*) Openness, Conscientiousness, Extroversion, Agreeableness, Neuroticism

[...] have previously written about American’s poor savings rates. Even the rich are only saving on average 12% of their income. The fact is that these poor [...]

i think it is unreasonable to expect that people in first two quintiles would save more.

Their basic needs are not met. Yes, you can be frugal and push yourself but it is not really worth it.

I think #4 is intermiddiate, i.e. could be both parents at work and only child care would cost 20K after tax. Another 30 K towards mortgage. So they do save some 6.2 is not bad + employers contribution…

I think what you find out that the whole philosophy and understanding of super savers is different. They typically pass non-return poin, when simply cannot spend money on a flash car or vacation.

Yes, they do live comfortable life but…

I am not a super saver. I think a lot of comes from insecurity and uncertainty. Even saving 50% of your after tax income will take you 20 years in a bad market to achieve financial independence. There is a chance that one would miss 20ties, 30ties…perhaps some 40ties as well….

There is only one secret I know of – earn more…

[...] rate is simply how much of your disposable (after tax) income that you save. Americans are abysmal savers, which probably explains why working longer is becoming the new [...]

[...] money is critical to achieving financial independence. As I’ve mentioned before, I’m not particularly [...]

[...] your career is something that I would strongly suggest. I’ve already written about how having a higher income will help you save more money, and the more money you save, the faster you can achieve financial independence. Yes, you could [...]

[...] people believe that Social Security will provide for them in retirement. And given America’s pathetic savings rate, Social Security is all that they’re going to have in retirement. Unfortunately, this means [...]