My Financial Independence Journey » Investing » Dividend Disaster Prevention and Recovery

Dividend Disaster Prevention and Recovery

Last week, I discussed several dividend disaster scenarios. Now that we’ve considered the worst, its time to prepare our defenses. Risk is inherent in every investment. Now that we understand some of those risks, we can explore various ways to prepare our portfolios against them.

Last week, I discussed several dividend disaster scenarios. Now that we’ve considered the worst, its time to prepare our defenses. Risk is inherent in every investment. Now that we understand some of those risks, we can explore various ways to prepare our portfolios against them.

If you haven’t done so yet, go back and read the article on dividend disasters. The below will make much more sense to you after you have some idea of what you’re defending against.

Doing Your Due Diligence

You thought homework was over when you graduated from college, didn’t you? Well, the homework is never over for a dividend growth investor. Regularly checking in on your stocks to make sure that their fundamentals are still sound is strongly encouraged. It can be hard to predict a dividend cut, but certain warning signs like ever increasing payout ratios, dropping earnings per share, and reductions in free cash flow or revenue can tip you off that things may not be on the up and up for a company.

Stopping Rules

Although my ideal period for holding an investment is forever, sometimes I must part ways with an investment and I must do it quickly. Like ripping off a Band-Aid. (*)

If a stock cuts it’s dividend, it needs to be sold immediately. You’ll lose some capital, but you won’t lose it all. Once the dividend cut is announced, the stock price tends to start dropping and keep on dropping. The sooner you can get out of a losing investment, the better you’ll be. Yes, you’re going to lose money by selling, you’ll just lose less money by selling earlier rather than later.

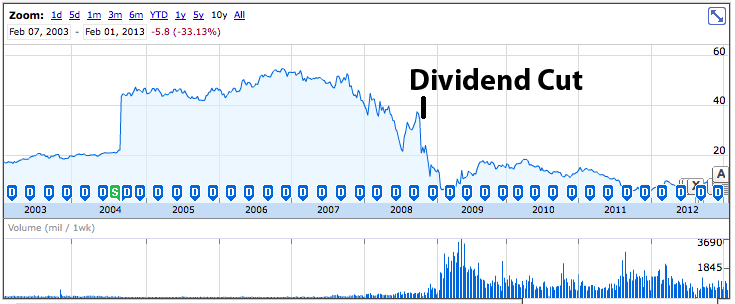

In addition to dividend cuts, any major materially adverse change in a company should be an indication to sell and sell quick. The quicker you sell the less capital you will lose. See the two examples below.

Example 1: Bank of America (BAC)

Example 2: BP

Reallocate Your Capital and Wait for Dividends to Grow

The nice thing about having a policy of investing in stocks with a history of increasing dividend payments is that you bet on the fact that all the dividends that weren’t cut are still growing. So how long would it take for each of the dividend cut scenarios described previously to regenerate their dividends?

Starting assumptions:

- We will begin with 2.5%, 5%, 10%, and 20% dividend cut scenarios.

- We want to know the amount of time it will take for the dividend stream to rise back to $40,000 per year.

- We’ll assume no inflation to make the math easy.

- We’ll also assume that you do not reinvest any capital, dividends, or other money. We want pure dividend growth only.

- We will assume dividend growth rates of 4%, 5%, 7% and 9% per year.

.

The interesting thing about the above chart is that in the worst case scenario, a 20% dividend cut and a paltry 4% growth rate, it will only take about six years for your dividend stream to regenerate itself. In the best case scenarios, it takes less than 1 year for the dividend stream to regenerate.

The Emergency Fund

In the event of substantial dividend cuts, you will likely need to replace the lost dividend income and you will need to do it quickly. This is why I strongly advocate having an emergency fund. I recommend that the minimum emergency fund be equal to either six months of living expenses or the price of a reasonable used car. Whichever is greater. Personally, I want to have one full year’s worth of expenses saved up in my emergency fund.

Alternatively, you could skip the emergency fund entirely, if you are appropriately diversified and have income in excess of what you need to live off of (see below).

Diversification

By now, you should be convinced of the importance of diversification. Indeed, you should be diversifying everything in order to have the maximum protection against dividend disasters.

1. Diversify your dividend growth holdings. As I illustrated previously, a 40 stock portfolio is much more resilient to a single stock dividend cut than a 10 stock portfolio. As you are increasing your dividend stock holdings, try to spread them out equally over all 10 S&P500 sectors. The more concentrated you are in a given sector, the more susceptible you are to a loss of dividend income when that sector encounters weakness. See the financial sector during the Great Recession.

2. Diversify your brokerage accounts. Since brokerages can fail, it’s a good idea to spread your holdings out over multiple brokerage firms, that way if failure does happen, all of your holdings will be appropriately insured and less of your dividend stream will knocked out as the brokerage failure is sorted out.

3. Diversify your income streams. I love dividend growth stocks, but there are plenty of other sources of revenue out there. Working a day job (full time or part time), freelance work, owning rental properties, and side hustles are all potential income streams. Depending on how sizable your dividend streams are compared to your expenses, it may behoove you to have some extra income streams active.

4. Diversify your investment categories. There are plenty of investment opportunities outside of dividend paying stocks. These include bonds, currency, commodities, real estate, peer to peer lending, cash (CDs and savings accounts), annuities, Treasuries, and others. All investment categories are not suitable for everyone. And there is no reason to invest in all the different categories right away. As your dividend portfolio grows and you come closer to financial independence or retirement, you may consider reducing your investment in stocks and increasing it into some of these other categories.

Excess Earnings

One of the best ways to buffer against dividend cuts is to produce larger income streams than you need to live on. When all is going well, you can spend or reinvest the excess dividends as you see fit. But when everything goes to hell and dividend cuts arrive, all those excess earnings will let you soak the damage done.

So how much excess do you need? Consider dividend cuts of 2.5%, 5%, 10%, and 20%, basically the spread of the dividend cut scenarios outlined above. The chart below illustrates how much extra dividend income you need and how large your portfolio must be in order to soak dividend cuts and still provide $40,000 a year in income to live off of.

.

Options: Puts to the Rescue

One often overlooked use for options is as a form of insurance. If you are afraid that a stock’s price may fall soon, you could buy a put option (called a protective put) you purchase a put option with a strike price that represents the minimum price that you want for the stock. If the price of the stock is below the strike price at the time of option expiration, the put option is exercised and the option owner will be forced to buy the stock from you at the agreed upon strike price. If the stock price is above the strike price at the time of expiration, then nothing happens. Either way, you are out the price you paid to buy the put option.

Of course, you need to be careful that the price you pay for the put option doesn’t eat up all the dividends that you are receiving from the stock.

(*) And much like ripping off Band-Aids, I’m still not very good at rapidly parting with losing stocks.

Disclosure: I am long BP and KO.

Readers: What are your plans to defend against dividend disaster scenarios?

Written by myfijourney

Filed under: Investing · Tags: dividend cut prevention

9 Responses to "Dividend Disaster Prevention and Recovery"

Leave a Reply to MFIJ Cancel reply

Nice article. Diversification is key, I’m targeting a 40 stock portfolio. It gets to be time consuming to keep up with much more than that. I’m sticking to stocks and real estate for now. I might diversify into bonds at a later time.

It’s worth mentioning that when you buy a put, you don’t have to wait until expiration to exercise your option. You can sell your shares any time before expiration. Also it’s the option seller that will be forced to buy, or “yourself”, the option buyer, will be forced to sell. It can get confusing.

I would like to get into real estate at some point. But I’ll probably have to look in another area since the market here looks difficult to easily make a profit being a landlord.

Very good article. As you say diversification is very important, but I think that in addition to the different types of diversification you mention, you have to keep in mind also the geographical diversification, not just rely on what you do a single country. For example, Europe is in crisis and many European shares have cut or eliminated their dividends, but in the U.S. the stock has continued to rise. It can happen that one day in the U.S. has fallen from shares strong suppression of dividends and other countries not. Therefore it is also important to diversify geographically.

I agree. One thing that I try to look it is how much of a company’s business comes from the US vs the rest of the world. Although, i’m not that knowledgeable in international stocks yet.

[…] lays out some very solid rules to prevent dividend disaster from hitting your […]

Nice write up. I think if you hold the stocks for years and the company cuts the dividend after 10 years of holding, if you sell immediately you won’t lose. Your stock over the thick times will be a lot higher then when you purchased it and dividends received over time will cover the drop and still you will have a lot left. So it is not a losing game. Of course if you have bought recently and three months later the company cuts its dividend, then yes you may see some red numbers. But others stocks in your portfolio should hold you above water.

That’s a good point. It kind of depend when the dividend cut happens vs when you bought the stock. It also depends how fast you sell the stock after the announcement. If you’re diversified enough, a given company cutting it’s dividend won’t be the end of the world for you.

[…] MFIJ from My Financial Independence Journey presents Dividend Disaster Prevention and Recovery […]

[…] post on Dividend Disaster Prevention and Recovery was featured in the Carnival of Personal FInance hosted by According to […]