My Financial Independence Journey » Stock Analysis » Norfolk Southern (NSC) Dividend Stock Analysis

Norfolk Southern (NSC) Dividend Stock Analysis

Norfolk Southern is a railroad service operating in the Eastern US and in parts of Canada. We tend to forget about railroads, but they do provide us with very important infrastructure for industry and commerce. Transport of coal primarily from mines to power plants accounts for about 31% of NSC’s revenue. Transport of general merchandise (all that crap you and I buy) comprises about 50% of NSC’s revenue. The general merchandise category also includes chemicals and automobiles. NSC serves 24 automobile manufacturing plants. The other 19% of revenues are derived from NSC’s intermodal business, a fancy term for standardized containers.

Norfolk Southern is a railroad service operating in the Eastern US and in parts of Canada. We tend to forget about railroads, but they do provide us with very important infrastructure for industry and commerce. Transport of coal primarily from mines to power plants accounts for about 31% of NSC’s revenue. Transport of general merchandise (all that crap you and I buy) comprises about 50% of NSC’s revenue. The general merchandise category also includes chemicals and automobiles. NSC serves 24 automobile manufacturing plants. The other 19% of revenues are derived from NSC’s intermodal business, a fancy term for standardized containers.

Basic Company Stats

- Ticker Symbol: NSC

- PE Ratio: 12.15

- Yield: 3.0%

- 5 year revenue growth (2007-2011): 4.3%

- % above 52 week low: 49.2%

- Beta: 1.06

- Market cap: $19.2B

- Website: www.nscorp.com

NSC vs the S&P500 over 10 years

NSC has been delivering solid capital gains for investors over the last 10 year period. By the end of 2012 an investment in NSC would have risen by 200%, compared to just over 50% for the S&P500.

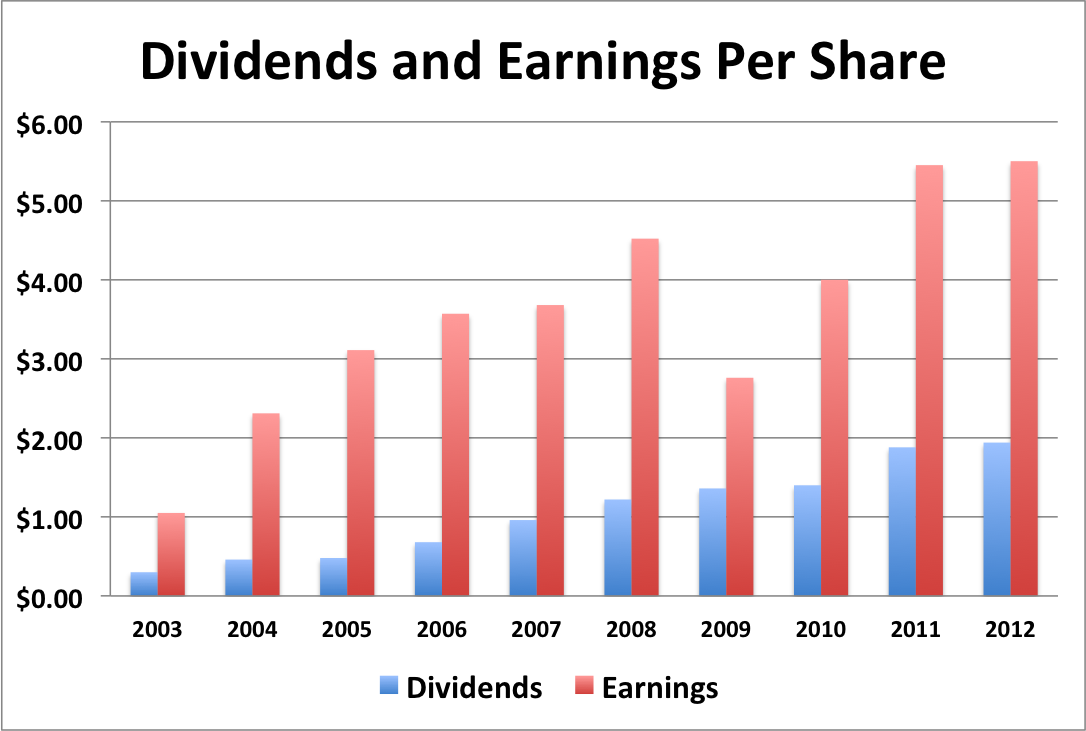

Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: 5.0%

- 10 year EPS growth: 20.2%

- 5 year dividend growth: 12.3%

- 10 year dividend growth: 23.0%

EPS took a hit in 2009, but has bounced back. EPS remains substantially higher than the dividend payout, leaving lots of room for continued dividend growth. The 5 year EPS growth has lagged the 5 year dividend growth, but the 10 year EPS and dividend growth rates are about equal.

As the economy recovers, EPS growth may increase given that about 70% of NSC’s revenues come from transporting consumer goods or the raw materials used to make those goods. Another potential benefit to NSC’s earnings would be rising fuel prices, which would make NSC more competitive vs long haul trucking.

With a dividend growth rate of 12.3% and a current yield of 3.2%, NSC’s yield on cost will grow to about 9.2% after 10 years.

Payout Ratio

With the exception of 2009, NSC’s payout ratio has remained below 40%. The payout ratios for 2010, 2011, and 2012 have been between 34% and 35%. The average payout ratio over the last 10 years has been 29%. The lower the payout ratio, the more available cash that the company has to continue to increase dividends or make capital investments.

Cash Secured Puts

Given that NSC is in the middle of it’s 52 week range, I’m hesitant to sell long-term puts against it. But if the economy keeps moving upwards, these might not be a bad option.

Risks

Competition-wise, railroads are an oligopoly, so they don’t really compete with other railroad companies. But that doesn’t mean that there isn’t competition for shipping. Goods can be shipped sea, by long haul trucking, or by pipeline. If fuel prices rise, it is likely that rail shipping will become more in demand. If fuel prices drop, then trucking becomes more competitive. Over the short-term, I don’t know what will happen with fuel prices, but over the long term, these prices will probably trend upwards, creating increased demand for rail shipping.

NSC has been investing heavily in its intermodal (shipping containers) transport business. If economic conditions continue to improve, then there will be a greater demand for consumer good and more use of railways.

Also, as companies attempt to reduce their carbon footprint they may begin to favor rail use over trucking. However, most of the chatter about carbon footprints is just that, chatter. The main driver of increased rail use will be fuel prices.

Conclusions

I like NSC. I think it is currently undervalued, has a respectable entry yield, a low PE ratio, and a low payout ratio with plenty of room for dividend growth. I would consider adding shares of NSC to my portfolio.

Disclaimer: I am currently short on NSC (one outstanding long term put).

Readers: What are your opinions about Norfolk Southern?

Written by myfijourney

Filed under: Stock Analysis · Tags: analysis, NSC

11 Responses to "Norfolk Southern (NSC) Dividend Stock Analysis"

Leave a Reply

Very interesting numbers here. The P/E is a getting on the high side for my buy preferences, but I like the payout ratio and dividend growth history. Goods coming from Asia or within North America need to get to their destination. Fuel costs rise making trucks a high cost alternative. Really, only rail is a reasonable transport alternative for long distance shipping. I will investigate this one further

From me, BMO – Bank of Montreal i- s my current big long position; just bout some more today.

I wish I would have bought NSC a few weeks ago. The price has really shot up lately.

I read about NSC somewhere and added it to my watch list. It is a good company (based on the numbers). I also like that the company pays dividends since 1901 and has a history of 11 years of consecutive dividend increase. Isn’t that a great sign of a healthy company!? If I had more cash I would be buying, but I do not have more cash, so I have to wait when I save more and then buy later. Thanks for publishing your analysis, it helps me to add more info into my own data and make sure whether I really want to buy this stock or not. Analysis of others help me to confirm my research or add to it. Thanks.

Martin,

I’m glad that my analysis was helpful. I’m hoping to do one every Monday if possible. And as I do more, I’m trying to make each one a bit better than the last.

Nice analysis. I hadn’t heard too much about Norfolk Southern before, but I’ve been interested in rail ever since Buffets purchase of Burlington. Rail definitely has a regional or area specific moat in my view and benefits from economic growth and spikes in oil price, both of which we are likely to see over the next few years. Overall, things look good for Norfolk . I’ll be looking to investigate further with a view to initiating if the price comes down a little more.

Integrator,

As the economy grows I expect NSC’s price to appreciate. It’s really shot up in the last few weeks and I’ve been chasing it but never managing to actually initiate a position. I’m really attracted to the area specific moat and the fact that rail works as a shipping alternative as gas prices rise. Rising gas prices seems inevitable to me, it’s only a question of rate of rise at this point.

I have also been looking at NSC recently and have a generally favorable opinion of it. However, one of the things that concerns me is that analyst estimates for current year and next year continue to tick down every month or so. I don’t make long term decisions based on stuff like that, but I’d like to know why this is happening, as it makes me concerned that there might be a factor I am not considering.

S.B.

Thanks for stopping by. I’m not sure about analyst’s estimates myself. They may have overshot in their initial estimations. Or NSC might not be doing as well as they hoped. This is pure speculation but.. the winter has been warmer on average, so possibly less need for the transport of coal for power plants. Also, the economy remains sad, so maybe there is less demand for stuff. Both of these could cause NSC’s earnings estimates to be reduced.

Great analysis. Many people ignore the importance of rail in the U.S. It’s a very stable industry so the dividends should continue for years. Norfolk Southern is definitely the way to go because it is one of the dominant players in the rail industry.

Brett,

Thanks for stopping by. Until I started looking into dividend growth investing, I was one of those people who underestimated the importance of rail.

[...] heavily involved in the transport of coal, general merchandise, chemicals and automobiles. See my recent analysis of NSC for more [...]