My Financial Independence Journey » Stock Analysis » Leggett & Platt (LEG) Dividend Stock Analysis

Leggett & Platt (LEG) Dividend Stock Analysis

Leggett and Platt is diverse manufacturer of components used in home furnishings, store and office fixtures, and cars and other machinery. The company has three main business areas. 1) The residential furnishings segment manufactures components used by mattress and furniture manufacturers. In fact, there is a good chance that your mattress has Leggett and Platt springs in it. 2) The commercial fixturing and components segment sells components for store fixtures and office seating. 3) The industrial materials segment manufactures wires and tubes for use in cars and other machinery.

Leggett and Platt is diverse manufacturer of components used in home furnishings, store and office fixtures, and cars and other machinery. The company has three main business areas. 1) The residential furnishings segment manufactures components used by mattress and furniture manufacturers. In fact, there is a good chance that your mattress has Leggett and Platt springs in it. 2) The commercial fixturing and components segment sells components for store fixtures and office seating. 3) The industrial materials segment manufactures wires and tubes for use in cars and other machinery.

Basic Company Stats

- Ticker Symbol: LEG

- PE Ratio: 22.52

- Yield: 4.14%

- 5 year revenue growth (2007-2011): -4.1%

- % above 52 week low: 96.9%

- Beta: 1.2

- Market cap: $3.8B

- Website: www.leggett.com

Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: 14.2%

- 10 year EPS growth: 1.9%

- 5 year dividend growth: 3.8%

- 10 year dividend growth: 8.9%

EPS took a huge hit in 2007. While earnings have recovered a bit, they remain only slightly higher than the dividend payout. In 4 of the last 6 years, EPS was less than the dividend payout. If this trend continues, it does not bode well for the future sustainability of the LEG’s dividend – in other words, a dividend cut may be immanent.

Leggett and Platt is a dividend aristocrat, meaning that this company has managed to consistently raise it’s dividend for at least 25 consecutive years. I would expect that there is great pressure for the company to continue the trend of rising dividends. However, the 5 year dividend growth rate is only 3.8%. With a growth rate of 3.8% the dividend will double in about 19 years. I suspect that if the dividend payout does continue to grow, that the growth rate will continue to slow.

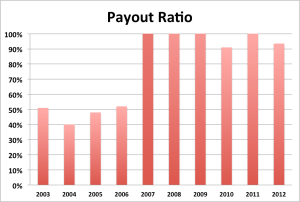

Payout Ratio

In 2007, when earnings tanked, the payout ratio skyrocketed and has remained high even after several years into our so-called post recession recovery. In 2007, 2008, 2009, and 2011 the payout ratio exceeded 100%. In 2010 and 2012 the payout ratio exceeded 90%. The payout ratio over the last 10 years averaged 103%. Nothing about this scenario suggests that the current dividend is sustainable.

Cash Secured Puts

Given that I would not suggest purchasing LEG, I would not suggest writing long term cash-secured puts against it.

Risks

The main risk facing LEG is the incredibly high dividend payout compared to earnings. This does not leave much cash left over to pay for capital improvements or acquisitions. With 47% of LEG’s sales resulting from the residential furniture segment, continued profit depends on the state of the economic recovery, which is still lagging. I would even suggest that the state of the housing market is going to determine LEG’s fate. If people don’t begin to expand their households and buy more new furniture, it’s difficult to see how sales from this segment will be able to expand.

LEG makes components, not actual finished products, so it will be very difficult for them to simply increase their prices in order to increase their profit margins.

Furthermore, if the dividend is to be sustained in the face of weak earnings the company will have to either borrow money or sell off assets.

Conclusions

There is nothing about this company as it currently stands, except it’s high yield, that makes me comfortable about investing in it. The payout ratio has been too high for too long, the dividend growth rate is declining, the P/E ratio is above 20, and 5 year revenue growth is negative.

I would not consider initiating a position in LEG. Nor would I consider writing long-term cash-secured puts against it.

If you already own LEG, I would suggest considering any of the following:

- Selling it, taking capital gains, and redistributing your capital elsewhere.

- Writing covered calls. If the stock get’s called away, I would consider that a blessing.

- Buying a long-term put, as insurance in case of the announcement of a dividend cut and the inevitable drop in stock price that will follow.

Disclaimer: I have no long, short, or otherwise position in LEG, nor do I plan on initiating one in the near future.

Readers: What are your opinions about Leggett and Platt?

Written by myfijourney

Filed under: Stock Analysis · Tags: analysis