My Financial Independence Journey » Stock Analysis » Aflac (AFL) Dividend Stock Analysis

Aflac (AFL) Dividend Stock Analysis

Aflac (AFL) is an insurance company that sells voluntary supplementary insurance policies in the US and Japan. Sales in Japan account for approximately 77% of Aflac’s revenue, with the US pulling in the other 23%. In Japan, Aflac mainly sells a variety of health insurance (these cover areas not included in the national health insurance), life insurance, and annuity products. These products are sold at over 90% of the banks, and at over 1000 post offices (yes, post offices in Japan sell lots of non-postal products). In the US, Aflac predominantly sells health and disability insurance. Most of Aflac’s US products are sold as part of employer sponsored group insurance plans.

Aflac (AFL) is an insurance company that sells voluntary supplementary insurance policies in the US and Japan. Sales in Japan account for approximately 77% of Aflac’s revenue, with the US pulling in the other 23%. In Japan, Aflac mainly sells a variety of health insurance (these cover areas not included in the national health insurance), life insurance, and annuity products. These products are sold at over 90% of the banks, and at over 1000 post offices (yes, post offices in Japan sell lots of non-postal products). In the US, Aflac predominantly sells health and disability insurance. Most of Aflac’s US products are sold as part of employer sponsored group insurance plans.

AFL Basic Company Stats

- Ticker Symbol: AFL

- PE Ratio: 8.36

- Yield: 2.80%

- % above 52 week low: 77.1%

- Beta: 1.66

- Market cap: $234.1 B

- Website: www.aflac.com

AFL vs the S&P500 over 10 years

AFL seems to be moving on par with the S&P500. After 10 years an investment in AFL would have increased by about 62%, compared to about 87% for the S&P500 as a whole. Not great, but not bad either.

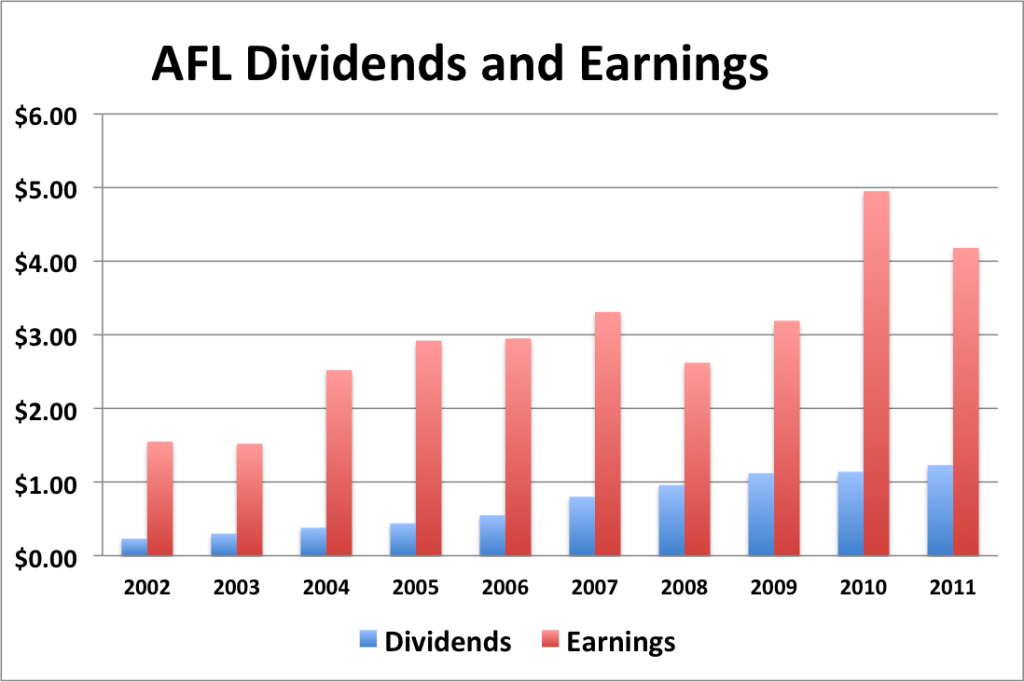

AFL Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: 6.0%

- 10 year EPS growth: 11.7%

- 5 year dividend growth: 11.4%

- 10 year dividend growth: 20.5%

EPS growth for AFL appears to be slowing down, maybe. In addition to the numbers above, the 3 year EPS growth was 14.5%, but the one year was -15.6% (both ending in 2011 as I don’t have complete data for 2012 yet). EPS for 2012 is estimated to be considerably higher at $6.63 per share. AFL’s dividend growth has been slowing down as well. The 10 year dividend growth rate is 20.5%, the 5 year growth rate is 11.4%, the 3 year growth rate is 4.8%, and the 1 year growth rate is 7.9% (all ending in 2011). AFL’s 2012 dividends grew 8.9% from 2011. So is this a slowdown or a speedup?

All of this requires some degree of explanation. Insurance companies make money by investing the premiums received by their policy holders. 2008 and 2009 were the height of the Great Recession, where almost all of investments fell off a cliff. Predictably EPS went down. Additionally AFL sells the majority of its products through employers. So as people lost their jobs in the Recession, they also stopped buy Aflac’s insurance. Aflac also had some investments in Europe, which if you’ve been watching the news at all over the last few years, you will recall has been flirting with economic collapse and default. Aflac has been working to “de-risk” its portfolio by moving its investments away from these riskier European assets, but this process has taken a toll on its earnings. Finally, there was the 2011 Tohoku tsunami, earthquake, and Fukushima nuclear disaster combination that hit Japan.

It is possible that as Europe stabilizes, Japan rebuilds after the disaster, the US pulls itself out of the recession, and the “de-risking” is complete that AFL’s EPS and dividends will begin accelerating again. It’s possible that the 2012 numbers are an indication of this. Of course, they could also be a one-off.

With a starting yield of 2.8% and a growth rate of about 9%, AFL’s yield on cost will grow to about 7% in 10 years. In order to double the dividend, using the rule of 72, it will take approximately 8 years.

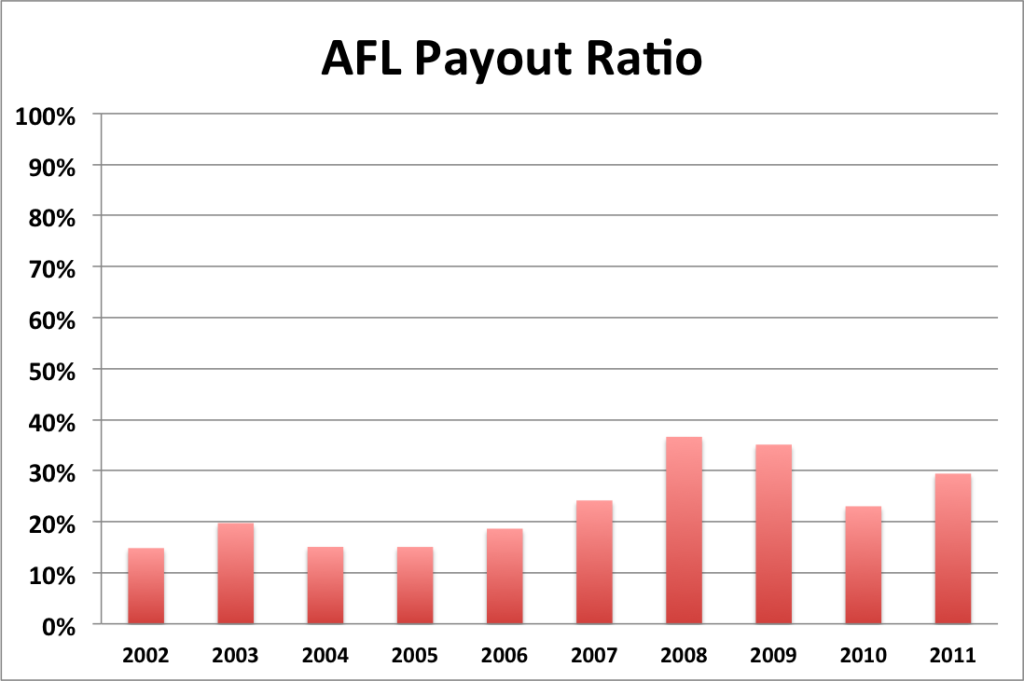

AFL Payout Ratio

AFL’s payout ratio has remained consistently low. Only topping 30% twice, during 2008 and 2009. The average payout ratio from 2002 to 2011 is 23%. Based on earnings estimates, it does not appear that the 2012 payout ratio will be much different. The low payout ratio leaves plenty of room for AFL to grow its dividends in the future.

AFL Revenue Growth

- 10 year revenue growth: 8.9%

- 5 year revenue growth: 9.6%

- 3 year revenue growth: 10.2%

- 1 year revenue growth: 6.9%

AFL has been consistently increasing its revenue over the last 10 years (up to 2011). 2012 estimates suggest that revenue will continue to grow at a nice clip as well. Increasing revenue means means increasing earnings and thus room to increase dividends.

AFL Balance Sheet

The current debt to equity ratio for AFL about 25%, which is much lower than other equities (~40%). The debt to equity ratio has increased a little over the last few years, but not enough to make me worry, as it is still well below the industry average.

AFL Risks

The main risk to Aflac is its exposure to potentially risky European investments. However, the company has been working to divest itself of these, but has been paying the price in reduced earnings. Due to its substantial Japanese exposure, the dollar/yen exchange rate could also be another source of risk for Aflac, should the yen drop in value compared to the dollar.

AFL Valuation Panel

Graham Number

The Graham number represents one very simple way to value a stock. The Graham number for AFL is $68.53. The current stock price is well below that, suggesting that AFL may be undervalued at the moment.

Two Stage Dividend Discount Model

Using a risk free rate of 2%, an expected return of 10% and the beta of 1.66, the CAPM model provides a discount rate of 13.3%. Using an initial growth rate of 9% for 5 years and a slower growth rate of 7%, the two stage model produced a value of $11.28 I also tried this model with a discount rate of 10% and got $55.92.

Gordon Growth Dividend Discount Model

Using the 23.3% discount rate, this model returns a value of $9.92. Using a more conservative 10% discount rate we get a value of $71.93.

Valuation Conclusion

Of the five different models tested, the median value is $68.53, which is higher than AFL’s stock price suggesting that it is undervalued at the moment.

AFL Cash Secured Puts

I have mixed opinions about selling puts AFL. On one hand the company may be undervalued in the long run, so selling long term puts against it might not be a bad idea. But AFL as well as the market appear overvalued at the moment so there is always the chance that you will be assigned the stock if the market corrects.

Conclusions

Overall, I like Aflac as a company and as an investment. I do feel that the company is attractively valued even though the yield is a bit lower than I would like. I would consider adding to my position in Aflac.

Disclosure: I am currently long AFL.

Readers: What are your opinions about Aflac?

Written by MFIJ

Filed under: Stock Analysis · Tags: afl, aflac, analysis

23 Responses to "Aflac (AFL) Dividend Stock Analysis"

Leave a Reply

Nice writeup MFIJ! I am long on AFL and believe they will continue to rid themselves of the European headache. With ample room to continue to grow the dividend should revenue growth take a hit, I think they have the potential to be solid long-term dividend growth holding.

Thanks! I’m with you, I think that AFL is going be a great long term buy. I am long AFL. I originally bought it during the first round of debt ceiling idiocy. I also sold an AFL put back then which worked out very well.

I picked up some shares earlier this year and have an open put against them. When selling puts you need to make sure the price if executed is at a level you’re comfortable paying. I’m happy with my put because it’ll give me ~10% return or a 3.00% YOC with almost a 5% reduction in my cost basis. Sounds like a win to me. Although I do hope that we get some kind of a correction soon. I’d love to make some more buys to keep increasing my dividends. Nice analysis on AFL. I’m curious how much P/B is useful for insurance companies since it’s typically a good metric for other financial institutions.

Just curious, where’d the 23.3% discount rate come from in the Gordon Growth DDM? That seems a little high.

I agree with you regarding puts. I try to calculate out the price stock price minus the options premium plus the commission and see if that will give me a reasonable starting yield or not.

I got the 23.3% discount rate by using the CAPM model to calculate it. I’ve been using CAPM for a little while, but I’m not convinced that it produces a better discount rate than just picking a standard 10%.

Same here. I feel that AFL is attractively valued, but the yield is lower than I wish. Good article on how their cash being held (an asset) is recorded as a liability per GAAP rules: http://seekingalpha.com/article/1032911-aflac-s-hidden-source-of-value

Thanks for stopping by. And thanks for the article tip!

I am looking to get into a couple insurance stocks at the moment if only I had unlimited capital to deploy

I know what you mean about always wishing that I had more capital. I’m usually stuck in a position where I have to pick just one out of a list of good companies. I always feel bad about those I passed up.

Aflac is one of my favorite and largest holdings. I’d be buying more at these levels but it already makes up the largest position in my portfolio so I want to spread some risk around by buying some other attractively valued companies if I can find some. I agree the starting yield is lower than most dividend investors would probably prefer but I think the growth will make up for it through the years.

Judging by the comments, AFL seems to be much loved by dividend growth investors. At this point, I think I own enough AFL, but I think that it’s a great stock and I’m pretty confident that it has some solid dividend growth in its future, especially as it gets its assets cleaned up.

[...] Continue reading [...]

Insurance companies are relatively cheap these days because of low interest rates. For some reason US financial firms are more undervalued than Canadian ones :0) AFL has underperformed the Dow for the last 5 years but I think it will outperform the market in the long run I have it on my watch list for sure. Maybe I’ll buy some later this year

I have it on my watch list for sure. Maybe I’ll buy some later this year

It looks like there might be a correction in the works. You might want to jump on AFL if the price drops some more.

I’ve been circling AFL for a while now, but I haven’t pulled the trigger on it yet, because I’m wondering if the yen dropping against the US dollar will impact the short term valuation.

Translation: I’m hoping to get a little more of a bargain in the next year or so. I may be wrong of course; it wouldn’t be the first time I let a good fish get away.

Thanks for stopping by.

I wouldn’t spend that much effort trying to time the currency markets. I just try to buy whatever is the best valued stock I can find each month as capital hits my account.

MFIJ,

Good writeup on AFL here.

I like the company, and it’s one of my larger positions at 100 shares (same position size as you). It’s currently one of my best ideas, and if I didn’t already own 100 shares I’d be actively looking to either build a position or add to a position on weakness. Great company.

Best wishes!

I agree. AFL is still a good company worth buying. But I’m comfortable with my current position size. If AFL has a massive price drop I might pick some more up.

Thanks for the in-depth analysis! The only thing I knew about Aflac is we have had at least 10 different Aflac salespeople come to our work and try to sell us plans!

Glad you liked the analysis! This one turned out to be a really popular one for some reason. I can’t believe the number of comments I’ve gotten on it. It must be the duck. Everyone loves ducks.

I would buy, most likely. I love reading these posts as it gives us good info as we save toward investing in dividend stocks. Thanks!

If AFL does dip a little bit I would consider buying more if I didn’t already have a considerable position in it. I’m glad that you like the analyses. My goal is to do one every Monday, although I might take some holidays off.

I really wish I had more capital to invest. AFL sounds really appealing.

Marissa,

Thanks for stopping by! I always wish that I had more capital to invest. Just save what you can and you’ll build your portfolio faster than you think.