My Financial Independence Journey » Stock Analysis » Automatic Data Processing (ADP) Dividend Stock Analysis

Automatic Data Processing (ADP) Dividend Stock Analysis

Automatic Data Processing (ADP) is the largest global provider of payroll outsourcing services and has over 570,000 clients worldwide. ADP also provides outsourcing services for human resources, tax filing, and benefits administration. ADP is divided into two main business segments, 1) employer services which focuses on payroll, human resource, benefits administration, time and attendance, and tax filing and reporting services. 2) Dealer services which focuses on transaction systems, data products and professional services to automobile and truck dealers and manufacturers. In 2006 ADP sold off it’s claims processing unit and in 2007 it spun off it’s brokerage services unit in order to focus more on its core business.

Automatic Data Processing (ADP) is the largest global provider of payroll outsourcing services and has over 570,000 clients worldwide. ADP also provides outsourcing services for human resources, tax filing, and benefits administration. ADP is divided into two main business segments, 1) employer services which focuses on payroll, human resource, benefits administration, time and attendance, and tax filing and reporting services. 2) Dealer services which focuses on transaction systems, data products and professional services to automobile and truck dealers and manufacturers. In 2006 ADP sold off it’s claims processing unit and in 2007 it spun off it’s brokerage services unit in order to focus more on its core business.

Automatic Data Processing Basic Company Stats

- Ticker Symbol: ADP

- PE Ratio: 21.5

- Yield: 2.8%

- % above 52 week low: 93.1%

- Beta: 0.7

- Market cap: $29.6 B

- Website: www.adp.com

ADP vs the S&P500 over 10 years

ADP has roughly paralleled the S&P500 for the last decade. By the end of 2012 an investment in ADP would have increased by about 100% compared to about 78% for the S&P500 as a whole.

ADP Earnings Per Share (EPS) & Dividend Growth

- 5 year EPS growth: 6.4%

- 10 year EPS growth: 5.9%

- 5 year dividend growth: 9.0%

- 10 year dividend growth: 13.9%

EPS for Automatic Data Processing have been rising steadily at around 6%. Similarly, ADP’s dividends have also been rising, but much faster. Currently it appears that dividend growth is slowing down a bit and may be flattening out around 7%. The 10 year dividend growth rate was 13.9%, the 5 year growth rate as 9.0%, the 3 year growth rate as 7.2%, and the one year growth rate is 7.9%. Given that dividend growth can’t exceed EPS growth forever, this trend makes sense.

With a starting yield of 2.9% and a growth rate of about 7.5%, ADP’s yield on cost will grow to about 7-8% in 10 years. In order to double the dividend, using the rule of 72, it will take approximately 10 years.

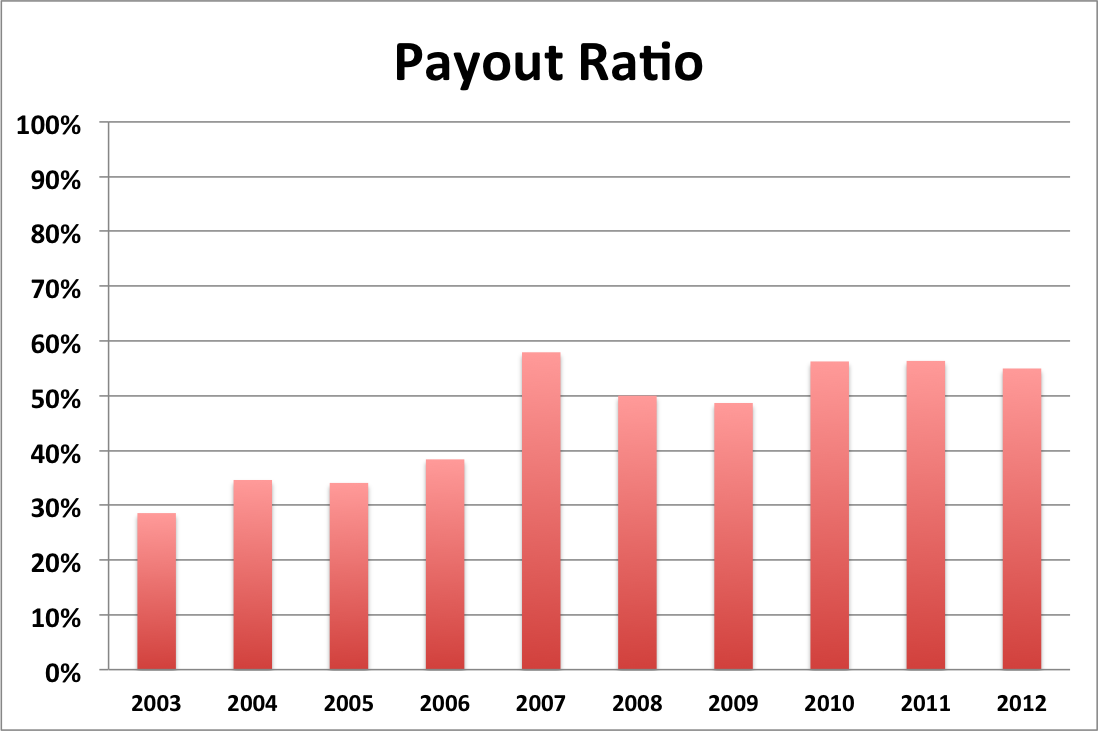

ADP Payout Ratio

ADP’s payout ratio has been steadily rising over time and is currently below 60%. The average payout ratio over the last 10 years was 46%. For the last three years the payout ratio has been hovering around 56%. I consider this acceptable, but would prefer it to be lower.

ADP Cash Flow Per Share and Revenue

- 10 year revenue growth (2003-2012): 4.5%

- 5 year revenue growth (2008-2012): 5.0%

- 3 year revenue growth (2010-2012): 9.7%

ADP has consistently produced positive and gradually increasing cash flow per share over the last 10 years. Revenue growth also remains strong and appears to be accelerating. If revenue and thus earnings continue to accelerate, it is possible that dividend growth may pick up again.

The cash flow spike in 2006 was the result of the sale of ADP’s claims services business.

ADP Balance Sheet

The current debt to equity ratio of ADP is 30%, which is about on par with other equities (~40%). ADP appears to have been aggressively paying off it’s debts over the last decade as the debt to equity ratio was 150% back in 2003. I consider this an encouraging sign.

ADP Risks

ADP currently has a solid hold on the payroll outsourcing marketplace. However, it should be noted that new companies are trying to enter this field, thus increasing competition.

As businesses continue the trend of outsourcing, I suspect that ADP will continue to be a major player in its field.

ADP Valuation Panel

Graham Number

The Graham number represents one very simple way to value a stock. The Graham number for ADP is $28.93. The current stock price is well above that, suggesting that ADP may be overvalued at the moment.

Two Stage Dividend Discount Model

Using a risk free rate of 2%, an expected return of 10% and the beta of 0.7, the CAPM model provides a discount rate of 15.6%. Using an initial growth rate of 7.5% for 5 years and a slower growth rate of 7%, the two stage model produced a value of $21.23. I also tried this model with a discount rate of 10% and got $58.07.

Gordon Growth Model

Since the dividend growth rate is flattening out around 7%, the average dividend growth rate of the dividend champions, I decided to try the Gordon growth model with both the 15.6% discount rate and a 10% discount rate. This model returned values of $19.78 and $59.34 respectively.

Valuation Conclusion

I feel that the simple one stage model is the best way to value ADP. However, the choice of discount rate heavily affects just how overvalued ADP appears to be. But all the models tested do agree that ADP is overvalued at present.

ADP Cash Secured Puts

ADP is a bit too overvalued at this time to sell long-term puts against it.

Conclusions

Overall, I like ADP as a company, but feel that it is slightly overvalued at present. I would consider initiating a position if the price drops enough for the PE ratio to go below 20.

Disclosure: Nothing to disclose

Readers: What are your opinions about Automatic Data Processing?

Written by myfijourney

Filed under: Stock Analysis · Tags: adp, analysis, automatic data processing

9 Responses to "Automatic Data Processing (ADP) Dividend Stock Analysis"

Leave a Reply

The time to pick up ADP was a year or two ago which is when I first started looking at it. I was very green at investing and DGI at the time so I didn’t jump on it. But that’s in the past so I can learn from it. I’d like to see it come down but I don’t know if it’ll be anytime soon where it gets grossly undervalued, fair value range would be acceptable though for a steady grower like ADP.

Thanks for the analysis!

Don’t remind me. I made the same mistake of not buying ADP back then and have been kicking myself for passing it up ever since.

I really like ADP as a company and would enjoying owning some shares. Unfortunately, like you I feel it is currently a little richly priced. I’d be interested in grabbing some shares if we see a market correction any time this year.

Dan Mac,

Thanks for stopping by.

I’m sure that they’re will be a market correction eventually. Maybe this year, maybe not. I’ll just keep ADP on my watch list until then and hope that I have some available capital for when the correction does happen.

I love ADP and plan on acquiring some when the price is right. As we move towards the digital age, this payment processor has positioned himself at the forefront of this new ear.

ADP is everywhere. I’m always amazed at just how many companies they handle payroll for.

I really like Paychex and ADP. I have more of a preference for Paychex given its higher yield, and ADP strikes me as more expensive. I think Paychex will benefit more from a sustained recovery given its exposure to small business who will like add more employees. Both should benefit from improvements in interest rates which will help improve the payroll processing cash float, one of the reasons earnings at both are a little down in my view.

I jumped into ADP during the recession and it’s been one of my better performing stocks since. The short term swings of ADP really seem to hinge on good/bad economic news so as long as things remain positive I don’t know that too big of a correction will come.

I wouldn’t worry about the short term swings. In the long run ADP should be a solid performer and will continue cranking out the dividends for years to come.